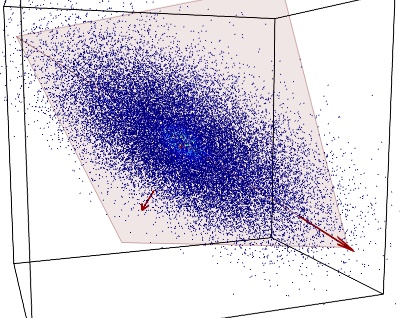

Back to basics: PCA on stocks returns

Principal component analysis Image from Gael Varoquaux blog

Back to basics: PCA on stocks returns

A short code snippet to apply PCA on stocks returns. No secret sauce is used here to clean the empirical covariance matrix. This blog post will mostly serve as a basis for comparing several flavours of PCA and their impact on ex-ante volatility estimation. We may look in future blog posts into Sparse PCA, Nonlinear PCA, Kernel PCA, Robust PCA, revisit our previous implementation of Hierarchical PCA (HPCA), and other techniques such as Independent Component Analysis (ICA).

from pathlib import Path

from datetime import datetime

import numpy as np

import pandas as pd

from tqdm import tqdm

from pandas.tseries.offsets import BDay

from sklearn.linear_model import LinearRegression

import matplotlib.pyplot as plt

sp500 = pd.read_csv('SP500_HistoTimeSeries.csv',

index_col='Date',

date_parser=lambda x: datetime.strptime(x, '%d/%m/%Y'))

sp500.index = pd.to_datetime(sp500.index)

sp500 = sp500.sort_index()

returns = sp500.pct_change()

returns = returns.clip(lower=-0.25, upper=0.25)

del returns['SPX Index']

NB_EIGEN = 5

LOOKBACK_WINDOW = 2 * 252

dates = returns.index[LOOKBACK_WINDOW:]

factor_covariances = []

factor_exposures = []

residual_vols = []

for date in tqdm(dates):

# compute the PCA on rolling past returns

past_returns = returns.loc[date - BDay(LOOKBACK_WINDOW):date]

past_returns = past_returns[(past_returns.count() > 100)

.replace(False, np.nan)

.dropna()

.index]

cov = past_returns.cov()

eig_vals, eig_vecs = np.linalg.eig(cov)

permutation = np.argsort(-eig_vals)

eig_vals = eig_vals[permutation]

eig_vecs = eig_vecs[:, permutation]

zeroed_returns = past_returns.replace(np.nan, 0)

factors = zeroed_returns @ eig_vecs.real

factors_5 = factors.iloc[:, :NB_EIGEN]

reg = (LinearRegression(fit_intercept=True)

.fit(X=factors_5, y=past_returns.fillna(0)))

B = reg.coef_

pca_returns = reg.predict(factors_5)

resid = past_returns - pca_returns

resid_vol = resid.std()

D = np.diag(resid_vol)**2

# factor covariance

fCov = (factors_5

.cov()

.rename(columns={i: 'E' + str(i) for i in range(NB_EIGEN)},

index={i: 'E' + str(i) for i in range(NB_EIGEN)})

.stack()

.reset_index()

.rename(columns={'level_0': 'factor_1',

'level_1': 'factor_2',

0: 'covar'}))

fCov['date'] = date

fCov = fCov.set_index(['date', 'factor_1', 'factor_2'])

# factor exposures

fExp = pd.DataFrame(B,

index=past_returns.columns,

columns=['E' + str(i) for i in range(NB_EIGEN)])

fExp['date'] = date

fExp = fExp.reset_index().rename(columns={'index': 'ticker'})

fExp = fExp.set_index(['date', 'ticker'])

# specific risk

spec_risk = (resid_vol

.reset_index()

.rename(columns={'index': 'ticker',

0: 'resid_vol'}))

spec_risk['date'] = date

spec_risk = spec_risk.set_index(['date', 'ticker'])

# save the factor covariance, exposures, and stocks specific risk

factor_covariances.append(fCov)

factor_exposures.append(fExp)

residual_vols.append(spec_risk)

factor_covariances = pd.concat(factor_covariances)

factor_exposures = pd.concat(factor_exposures)

residual_vols = pd.concat(residual_vols)

100%|██████████| 3470/3470 [24:27<00:00, 2.37it/s]

We save the factors covariance, exposures, and residual volatilities for future reuse:

Path("risk_model").mkdir(parents=True, exist_ok=True)

factor_covariances.to_parquet('risk_model/factor_covariances.parquet')

factor_exposures.to_parquet('risk_model/factor_exposures.parquet')

residual_vols.to_parquet('risk_model/residual_vols.parquet')

Loading the saved risk model components:

factor_covariances = pd.read_parquet('risk_model/factor_covariances.parquet')

factor_exposures = pd.read_parquet('risk_model/factor_exposures.parquet')

residual_vols = pd.read_parquet('risk_model/residual_vols.parquet')

factor_covariances.tail()

| covar | |||

|---|---|---|---|

| date | factor_1 | factor_2 | |

| 2016-07-29 | E4 | E0 | -0.000842 |

| E1 | 0.000078 | ||

| E2 | 0.000133 | ||

| E3 | -0.000007 | ||

| E4 | 0.002611 |

factor_exposures.tail()

| E0 | E1 | E2 | E3 | E4 | ||

|---|---|---|---|---|---|---|

| date | ticker | |||||

| 2016-07-29 | XEC UN Equity | 0.068088 | -0.108401 | 0.040181 | 0.003394 | -0.173384 |

| ZTS UN Equity | 0.037352 | 0.036895 | -0.015819 | -0.090589 | -0.037028 | |

| DLR UN Equity | 0.019566 | 0.026160 | 0.081157 | 0.001729 | 0.017967 | |

| EQIX UW Equity | 0.034544 | 0.045924 | 0.033238 | -0.006657 | -0.018939 | |

| DISCK UW Equity | 0.052699 | -0.012641 | 0.002077 | 0.010083 | 0.039095 |

residual_vols.tail()

| resid_vol | ||

|---|---|---|

| date | ticker | |

| 2016-07-29 | XEC UN Equity | 0.012693 |

| ZTS UN Equity | 0.013028 | |

| DLR UN Equity | 0.009801 | |

| EQIX UW Equity | 0.011945 | |

| DISCK UW Equity | 0.014904 |

We now apply the risk model through history on a long-only equally weighted portfolio:

backtest_dates = sorted(residual_vols.index.get_level_values(0).unique())

# long-only equally weighted portfolio

weights = pd.DataFrame(False, index=returns.index, columns=returns.columns)

for date in tqdm(backtest_dates):

weights.loc[date, residual_vols.loc[date, :].index] = True

weights = weights.astype(int)

weights = (weights

.div(weights.sum(axis=1), axis=0)

.replace(0, np.nan))

100%|██████████| 3470/3470 [02:30<00:00, 23.05it/s]

rets = (weights * returns.shift(-1)).sum(axis=1).loc[backtest_dates]

realized_vol = rets.rolling(63).std()

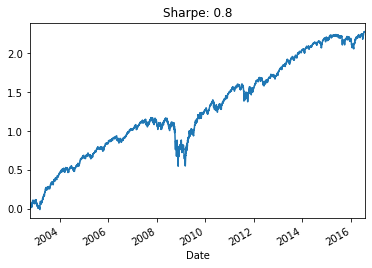

rets.cumsum().plot(

title=f"Sharpe: {round(rets.mean() * np.sqrt(252) / rets.std(), 2)}")

plt.show()

Performance and Sharpe ratio of the equally weighted long-only portfolio

pca_risk = []

for date in tqdm(backtest_dates):

w = weights.loc[date].dropna()

r = residual_vols.loc[date, :]

e = factor_exposures.loc[date, :]

c = (factor_covariances

.loc[date, :, :]

.reset_index()

.pivot(index='factor_1',

columns='factor_2',

values='covar'))

cov = e @ c @ e.T + np.diag(r.resid_vol**2)

risk = np.sqrt(w.T @ cov @ w)

pca_risk.append(risk)

pca_risk = pd.Series(pca_risk, index=backtest_dates)

100%|██████████| 3470/3470 [01:03<00:00, 54.44it/s]

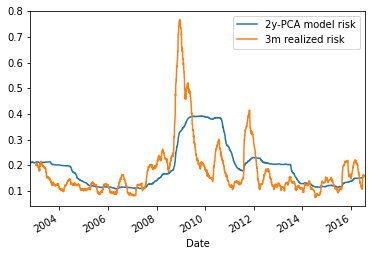

(pca_risk * np.sqrt(252)).plot( label='2y-PCA model risk')

(realized_vol * np.sqrt(252)).plot(label='3m realized risk')

plt.legend()

plt.show()

time series of the 3-month realized volatility (orange), and the *ex-ante* volatility (blue) given by the 2-year 5-factor PCA risk model

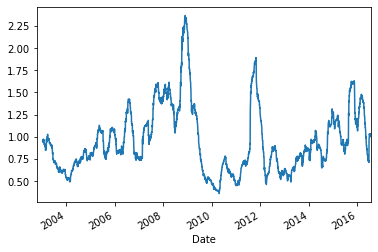

On average the 5-factor PCA risk model overestimates the risk by 5%:

(realized_vol / pca_risk).plot()

round((realized_vol / pca_risk).mean(), 2)

0.95

time series of the ratio between 3-month realized volatility over *ex-ante* volatility given by the 2-year 5-factor PCA risk model

We can see on the graph above that the 5-factor PCA risk model applied to such a simple long-only portfolio can be off by a factor 2 in case of extreme vol in the markets. Following a crisis, the risk model will be too conservative for a while… The duration of that period matches roughly the window length used for the PCA calibration (i.e. the rolling window size used to estimate the covariance between the stocks returns).