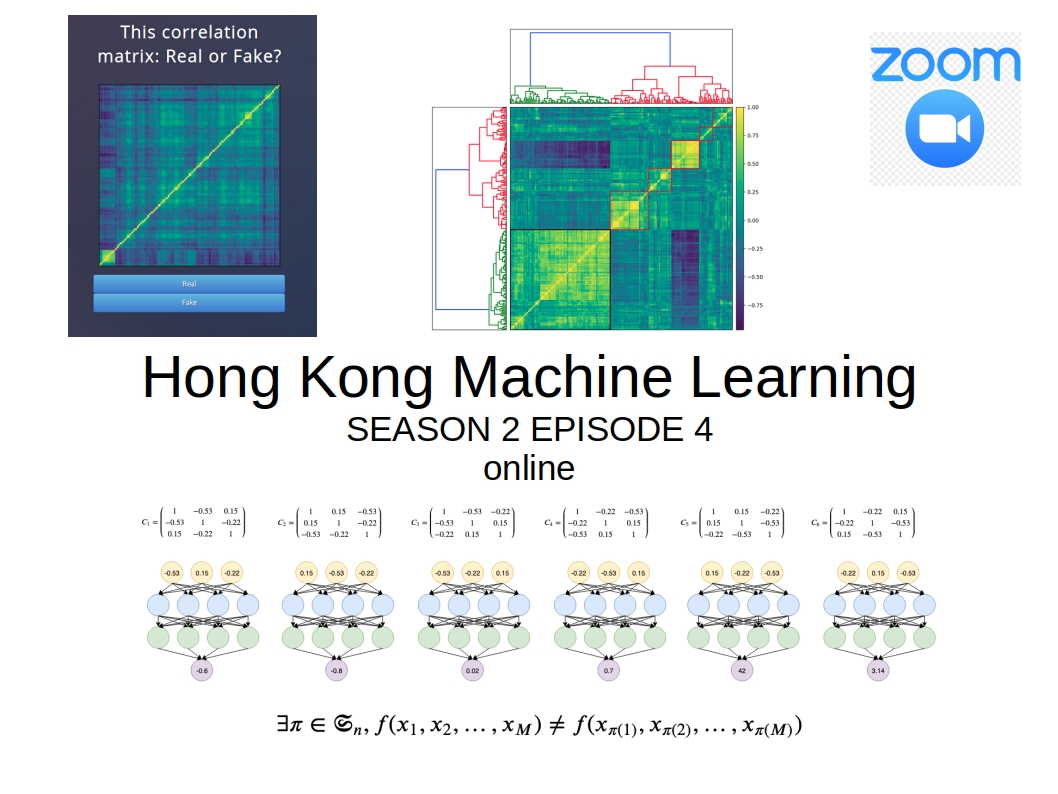

[HKML] Hong Kong Machine Learning Meetup Season 2 Episode 4

[HKML] Hong Kong Machine Learning Meetup Season 2 Episode 4

When?

- Wednesday, April 8, 2020 from 7:30 PM to 8:30 PM

Where?

- At your home, on zoom. All meetups will be online as long as this COVID-19 crisis is not over.

Since this online meetup was a first, I presented some of my research work to test the setting.

Programme:

Gautier Marti - My recent attempts at using GANs for simulating realistic stocks returns

Abstract

I will share my experience on using GANs for generating something else than natural images, in that case correlation matrices of stocks. I can see a few applications such as more valid comparisons of portfolio construction methods (e.g. MV vs. risk parity vs. de Prado’s HRP vs. HERC).

The slides for this talk can be found here.