Mind the Jensen Gap!

Mind the Jensen Gap!

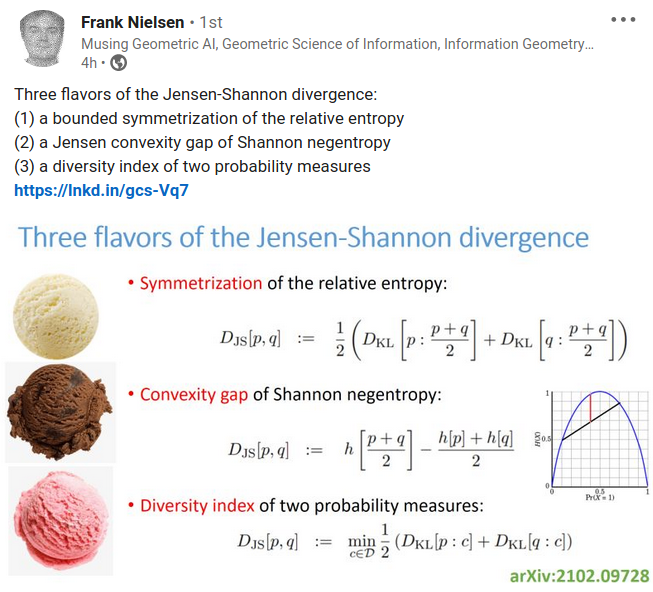

A post from my former PhD advisor Frank Nielsen popped up on my LinkedIn feed this morning mentionning the Jensen-Shannon divergence, and the convexity gap:

This convexity gap, the Jensen Gap, can have an (undesired) impact when you transform your features or target variables in a typical machine learning / data science pipeline.

When doing statistics or ML, we often normalize/standardize and apply other transformations on the original variables so that their distribution looks nicer and fits better the hypotheses required by the statistical tools (e.g. Gaussianization).

Let’s be a bit more concrete. Say you are trying to predict the fair price of goods sold on e-commerce platforms using regressions, i.e. essentially evaluating a conditional expectation.

Prices are (usually) positive and heavily right-skewed (you can always find very very expensive goods). To help with regressions, it is common to apply a log-transform on prices. This log-transform makes the resulting transformed variable (log-prices) roughly Gaussian. One does ML operations (e.g. taking expectations) in the log-space, before transforming back with the inverse bijective transform: exp.

The Jensen inequality reads, for $f$ convex:

That is, the Jensen Gap is $\mathbb{E}[f(Y)] - f(\mathbb{E}[Y]) \geq 0$.

Now, back to our toy-example, considering $Y$ the random variable for prices,

we have:

That is,

which means we would underestimate the real quantity.

We can illustrate that numerically. Let’s consider $Y \sim \text{ Lognormal}(\mu, \sigma^2)$. We know that $\mathbb{E}[Y] = \exp(\mu + \frac{1}{2}\sigma^2)$.

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

%matplotlib inline

mu = 4

sigma = 2

size = 500

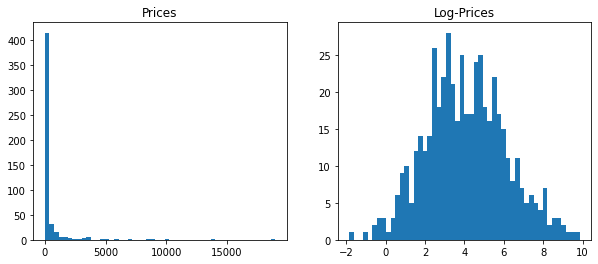

prices = pd.Series(np.random.lognormal(mu, sigma, size=size))

plt.figure(figsize=(10, 4))

plt.subplot(1, 2, 1)

plt.hist(prices, bins=50)

plt.title('Prices')

plt.subplot(1, 2, 2)

plt.hist(np.log(prices), bins=50)

plt.title('Log-Prices')

plt.show()

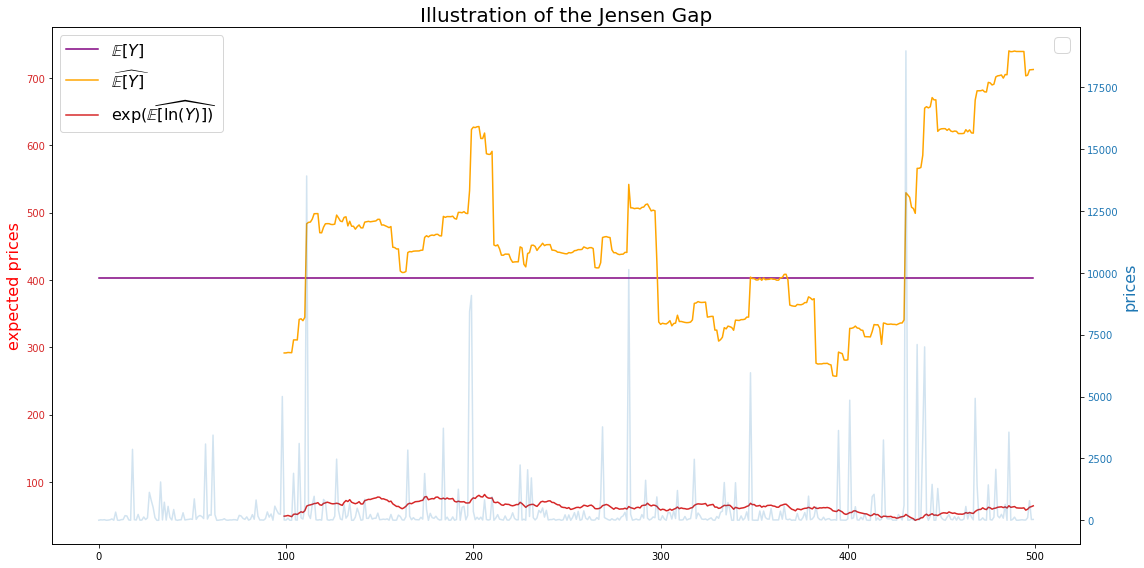

Let’s now compare the true mean, the estimated mean, and the estimated mean in the log-space converted back to the original space:

window = 100

fig, ax1 = plt.subplots(figsize=(16, 8))

color = 'tab:red'

ax1.set_ylabel('expected prices', color='red', fontsize=16)

ax1.plot(pd.Series([np.exp(mu + sigma**2 / 2)] * size),

label=r'$\mathbb{E}[Y]$', color='purple')

ax1.plot(prices.rolling(window).mean(),

label=r'$\widehat{\mathbb{E}[Y]}$', color='orange')

ax1.plot(np.exp(np.log(prices).rolling(window).mean()),

label=r'$\exp(\widehat{\mathbb{E}[\ln(Y)]})$', color=color)

ax1.tick_params(axis='y', labelcolor=color)

ax1.legend(fontsize=16)

ax2 = ax1.twinx()

color = 'tab:blue'

ax2.set_ylabel('prices', color=color, fontsize=16)

ax2.plot(prices, alpha=0.2, color=color)

ax2.tick_params(axis='y', labelcolor=color)

plt.title('Illustration of the Jensen Gap', fontsize=20)

plt.legend(fontsize=20)

fig.tight_layout()

plt.show()

True mean:

np.exp(mu + sigma**2 / 2)

403.4287934927351

Estimated mean (full sample):

np.mean(prices)

449.2386823126975

Estimated mean obtained after log-transform (full sample) and converted back with exp-transform:

np.exp(np.mean(np.log(prices)))

59.185451725779366

Question: Is it possible to have an idea of the expected gap in order to debias quantities?

In this particular example, we can notice that the gap is a function of $(\mu, \sigma)$; It seems that the larger $\mu$ or $\sigma$, the larger the gap.

Conclusion: Mind the gap!